30 April 2026

Global gambling market to exceed $1 trillion GGR by 2030, driven by online channel growth

H2 Market Data Update: IMF Data Extension to 2031

Global gambling market to exceed $1 trillion GGR by 2030, driven by online channel growth

Following the IMF's latest publication of its World Economic Outlook Database in April 2026, H2 has incorporated the updated GDP and inflation indicators into its global gambling market models. Notably, this release extended the IMF's forecasting horizon by one year, to 2031. Over the past week our team has worked the revised macroeconomic assumptions through the models covering all products and markets we track, and our full suite of summary datasets has been extended accordingly — adding a new 2031 forecast column across every product row and market.

The IMF's update represents a relatively modest set of revisions compared to prior cycles. While the April 2026 database reflects continued uncertainty around trade policy and the global macroeconomic outlook, the net effect on H2's gambling market forecasts is limited. At the global level, our forecast for total gambling GGR in 2030 has moved from $1,023bn to $1,031bn, an upward revision of less than 1%. These changes are broadly consistent across forecast years, with revisions of around 0.6%–0.8% for the period 2026–2030.

$1 Trillion GGR Milestone

The most significant headline from this update is the confirmation that global gambling GGR will cross $1 trillion for the first time in 2030, with H2 now forecasting total global GGR of $1,031bn in that year, rising to $1,088bn in 2031. To put this in context, global GGR stood at $438bn in 2015, meaning the industry will have more than doubled in nominal terms over a 16-year period. By 2024 the market had already reached $712bn, reflecting the rapid post-Covid recovery and strong structural growth in online gambling.

The primary driver of this growth is the online channel, which has grown from $89bn (20% of total GGR) in 2015 to $293bn (41% of total) in 2024, and is forecast to reach $530bn in 2030 (51% of total) and $568bn in 2031 (52% of total). Online gambling is therefore expected to account for the majority of global GGR for the first time in 2029, when it will represent 50.3% of the $979bn total. Land-based GGR, while continuing to grow in absolute terms, will account for less than half of global gambling revenue from that year forward, declining from an 80% share in 2015 to under 48% by 2031.

Product Split: Betting, Gaming and Lottery

Across all channels combined, gaming (encompassing casino, gaming machines, bingo and related products) remains by far the largest segment of the global gambling market, accounting for around $546bn of the forecast $1,031bn global GGR in 2030, or roughly 53% of the total. Betting (horserace and sports) will contribute approximately $305bn (30%), with lotteries accounting for the remaining $181bn (18%).

Within the online channel, the product dynamics are somewhat different. Online betting is currently the single largest online product, generating $148bn in 2024 (50% of total online GGR), driven by the rapid global expansion of sports betting — particularly in the United States, Latin America and Africa. However, online casino/iGaming is growing faster, reaching $233bn in 2030 versus betting at $248bn — narrowing the gap materially. By 2031, the two segments are virtually neck-and-neck, while online lottery remains a relatively modest but steady 6% of online GGR throughout the forecast period.

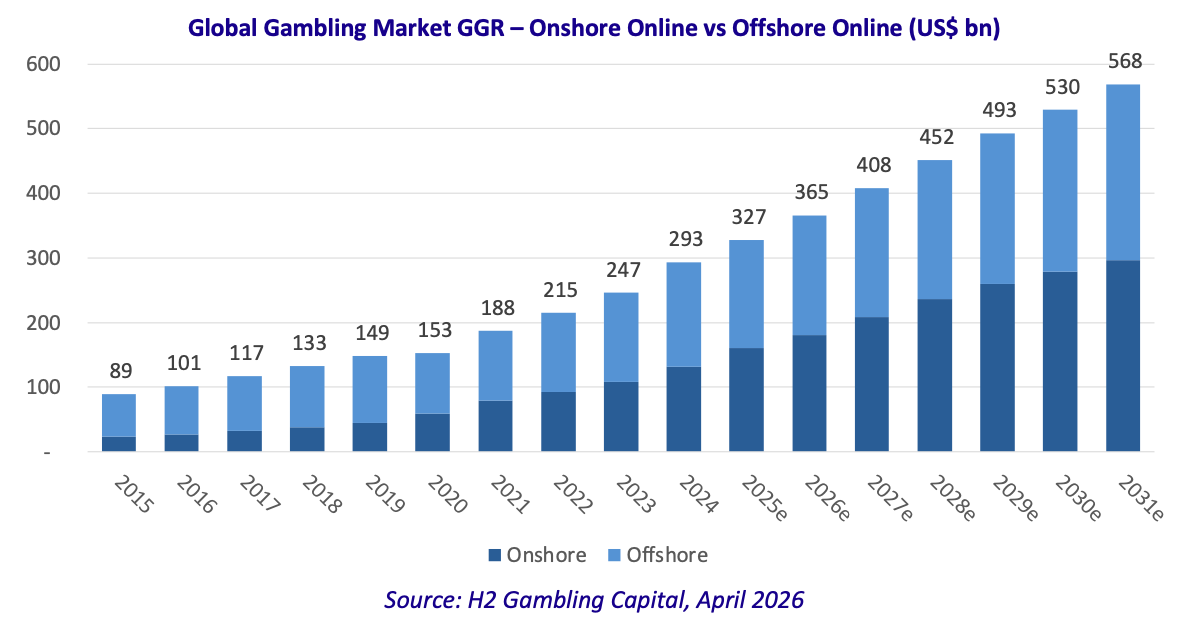

Onshore vs. Offshore Online

One of the more structurally significant trends captured in the updated H2 data is the shifting balance between onshore (regulated) and offshore (unregulated) online gambling. In 2015, the online market was overwhelmingly dominated by offshore operators, which accounted for approximately $65bn, or 73%, of global online GGR of $89bn. Onshore online — comprising markets where online gambling is formally licensed and regulated — represented just $24bn, or 27% of the online total.

Over the intervening decade, regulatory liberalisation across multiple jurisdictions — most notably the United States following the PASPA repeal, and across Latin America, with Brazil's market opening in 2025 — has driven a substantial increase in the onshore share. By 2024, onshore online GGR had reached $132bn, representing 45% of total online GGR of $293bn. Offshore, while continuing to grow in absolute terms, has seen its share compress significantly to 55%.

Looking ahead, H2's models project that onshore online will overtake offshore for the first time. This structural shift reflects ongoing global regulatory expansion, with numerous markets in various stages of licensing online gambling for the first time. The headwind to this is the continued growth of offshore GGR in absolute terms, with offshore GGR continuing to take share in a number of more mature markets.

Regional Breakdown

At a regional level, Asia and the Middle East remains the largest gambling region globally, accounting for $270bn in 2024 and projected to reach $398bn by 2030. Despite its scale, Asia & ME's share of global GGR is gradually declining as other regions grow faster, particularly North America and Latin America. North America is forecast to reach $284bn in 2030 (from $193bn in 2024), driven by continued expansion of regulated online betting and gaming in the United States and Canada. Europe is expected to grow from $177bn in 2024 to $236bn by 2030, with online channels continuing to account for a large and growing proportion of European GGR.

The highest rates of growth are concentrated in Latin America & the Caribbean and Africa, both of which are at earlier stages of market development and regulatory evolution. LatAm GGR is forecast to grow from $29bn in 2024 to $51bn in 2030, while Africa advances from $14bn to $31bn over the same period — in both cases driven primarily by online channel expansion. Oceania represents the smallest of the six regions at $28bn in 2024, growing to $33bn by 2030.

As with previous IMF updates, the forecasts are presented on a nominal basis, meaning a portion of GGR growth reflects currency inflation rather than real-terms expansion. H2's summary datasets allow subscribers to view each country's performance on an inflation-adjusted basis, providing a more granular view of volume growth versus price effects. Given that this IMF update did not materially revise global inflation expectations, the real-terms growth trajectory is broadly unchanged from the previous release.

FX Impact

All of H2’s forecasts in the main summaries are done on a constant FX basis – i.e. each individual market is forecast in local currency, and translated to USD / EUR at the current FX rate. The reason for this is that it is the best representation of underlying growth in the industry, rather than industry trends being disguised by the strengthening and weakening of the USD or EUR.

However, the downside to this is that it does not take into account future devaluation of currencies in high inflation markets. H2’s individual market datasets, and H2’s multi-currency global summary allows subscribers to view markets / the industry on a current FX basis – i.e. taking into account forecast devaluations of high inflationary markets. On that basis, in USD or EUR, future global market forecasts would be lower than on a constant currency basis.

PDF Download Available Here